City Attorney’s Office Addresses Issues Raised in City Council Meeting Regarding 353 Plan Amendment and to Provide Additional Information as Requested at the January 6, 2025, City Council Meeting

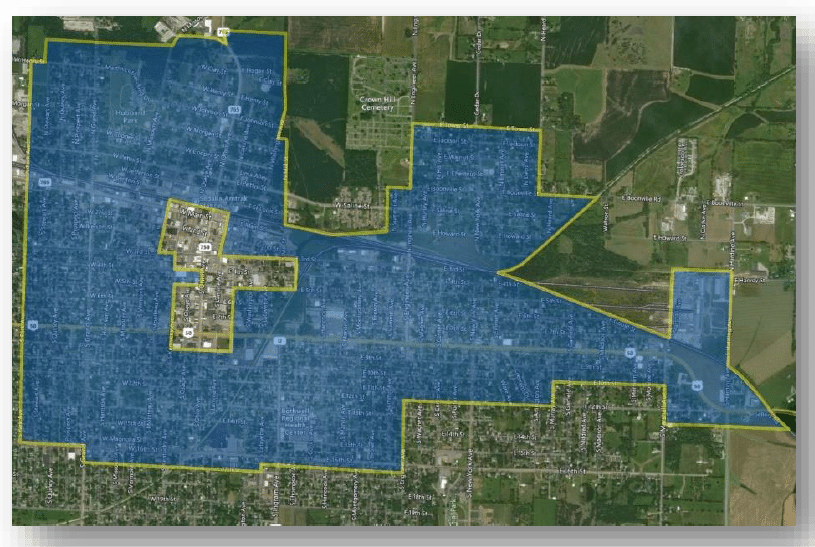

This message is from Joe Lauber, Sedalia City Attorney. — I would like to address issues raised in the City Council meeting held on Monday, December 16. The purpose of the public hearing and proposed ordinance on this topic at that meeting was to amend the Chapter 353 Redevelopment Plan Midtown Residential Area, which has been in place since it was approved by Ordinance No. 11168 on May 18, 2020, to add property that was excluded from the original plan. The area to be added can roughly be described as the downtown area, which is depicted as the “donut hole” in the map provided below.

During Council consideration of the agenda item, a question was raised by Councilman Oldham regarding how Chapter 353 tax abatement incentives work. An associate of the City Attorney’s office answered that tax abatement is not available under the existing plan. Unfortunately, this answer was incorrect for the reason that it was incomplete and did not address the full context of the program. Tax abatement can be granted pursuant to a redevelopment agreement between the City and a private property owner; provided that the property owner submits a development proposal and development plan in accordance with state statutes (Chapter 353, RSMo.) and the City’s ordinances (Section 42-31 through 42-54). We sincerely regret the confusion caused by our incomplete answer and appreciate that Mayor Dawson quickly recognized the concerns and postponed the vote until the next meeting so that the City Attorney’s office can provide a thorough explanation of 353 incentives generally and how the City’s existing plan works from a broader perspective.

353 incentives have been an economic development tool available to cities in Missouri for over 30 years. “353” refers to the chapter where these incentives can be found in the Revised Statutes of Missouri. This is the same area of state statutes where other types of corporations are addressed; for example, general business corporations are found at Chapter 351 and non-profit corporations are found at Chapter 355. Sedalia and other cities throughout the state utilize this very positive tool to financially assist property owners to make improvements to their properties. For cities to provide public funds to private property owners a public purpose must exist. Chapter 353 requires a city to make findings and declare an area blighted before funds may be provided.

Many 353 plans focus on tax abatements as their primary funding source. However, these abatements reduce tax revenues for all taxing jurisdictions in a redevelopment area like the school district, county, and city. Sedalia’s Chapter 353 Development Plan Midtown Residential Area does not make tax abatements the primary funding source for these incentives. Instead, the City of Sedalia has, over a period of years, budgeted City funds totaling approximately $500,000 for property owners in the redevelopment area to use to make improvements to their property with no impact on our neighboring taxing jurisdictions. I emphasize that tax abatements are available to property owners interested in seeking them, and the City has a process for those individuals to follow to obtain abatements, which in part will include a tax impact statement to be provided to affected taxing jurisdictions.

Participation in Sedalia’s 353 program, or any 353 program anywhere in Missouri is completely voluntary. Statements that this program are a “land grab” by the City are misguided and create false negativity about a very positive program. Projects funded by sources other than tax abatement do not require property acquisition by the City at all. If an applicant requests and is granted tax abatements, state statutes require the property to be sold to the 353 Corporation to trigger abatements. In these circumstances, the property is immediately sold back to the property owner as only a temporary transfer is required for tax abatements to begin.

I appreciate the Mayor’s quick action on Monday night to allow this matter to be more thoroughly discussed and our office looks forward to presenting additional information on the topic of 353 incentives in general and Sedalia’s Chapter 353 Development Plan Midtown Residential Area specifically at the January 6 meeting. — Kindest regards, Joseph Lauber